The Power Systems Research Truck Production Index (PSR-TPI) increased from 104 to 116, or 11.5%, for the three-month period ended June 30, 2022, from Q1 2022. The year-over-year (Q2 2021 to Q2 2022) loss for the PSR-TPI was 130 to 116, or -10.8%. The PSR-TPI measures truck production globally and across six regions: North America, China, Europe, South America, Japan and Korea, and Emerging Markets. This data comes from OE Link™, the proprietary database maintained by Power Systems Research.

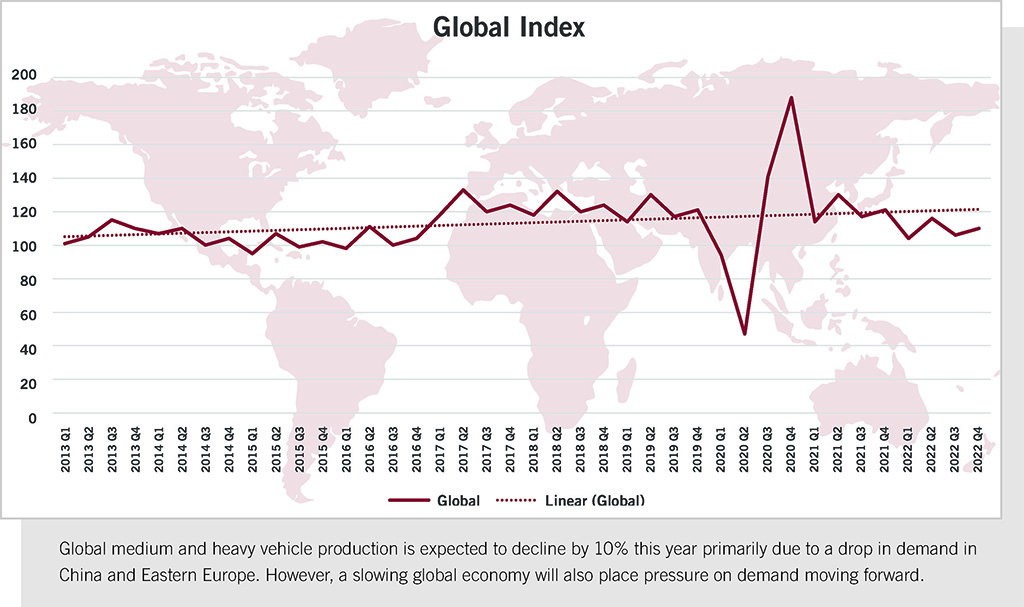

Global Index

Global medium and heavy vehicle production is expected to decline by 10% this year primarily due to a drop in demand in China and Eastern Europe. However, a slowing global economy will also place pressure on demand moving forward.

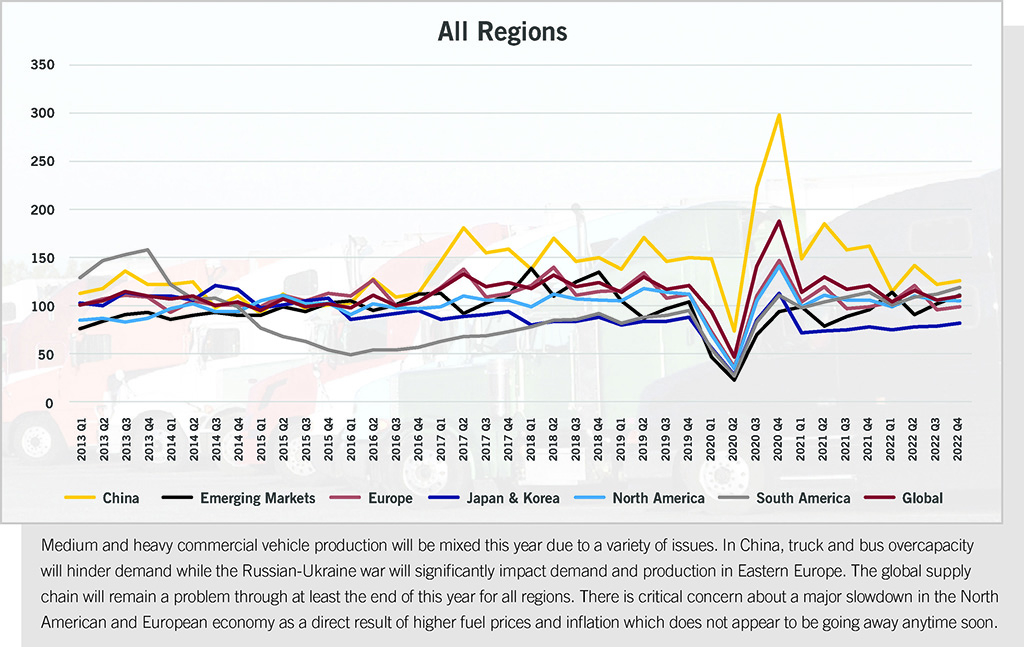

All Regions

Medium and heavy commercial vehicle production will be mixed this year due to a variety of issues. In China, truck and bus overcapacity will hinder demand while the Russian-Ukraine war will significantly impact demand and production in Eastern Europe. Global supply chains will remain a problem through at least the end of this year for all regions. There is critical concern about major slowdowns in the North American and European economies as a direct result of higher fuel prices and inflation which does not appear to be going away anytime soon.

North America

Medium and heavy commercial vehicle production is expected to increase by 4.7% this year over 2021 as OEMs continue to struggle with the supply chain disruptions that are expected to continue through at least the end of the year. However, the threat of an economic slowdown is increasing, primarily due to significantly higher fuel prices, increasing interest rates and overall inflation. Even with an impending economic slowdown, freight should remain strong through at least the first quarter of 2023 as the fleets continue to reduce supply chain backlogs.

Europe

European medium and heavy commercial vehicle production volumes will be mixed this year with higher demand in Western Europe and much lower demand in Eastern Europe. Production in Eastern Europe is expected to decline in many countries primarily due to the Russian invasion of Ukraine. Russian OEMs have continued to produce vehicles during the first half of the year but are hampered due to lower demand and low or inconsistent production rates due to significant supply chain constraints. Eastern European countries such as Kazakhstan, Lithuania and Uzbekistan will also see a production decline this year due, in part due to reduced truck kit assemblies coming from Russia. Ukrainian truck production has ceased through at least the remainder of the year.

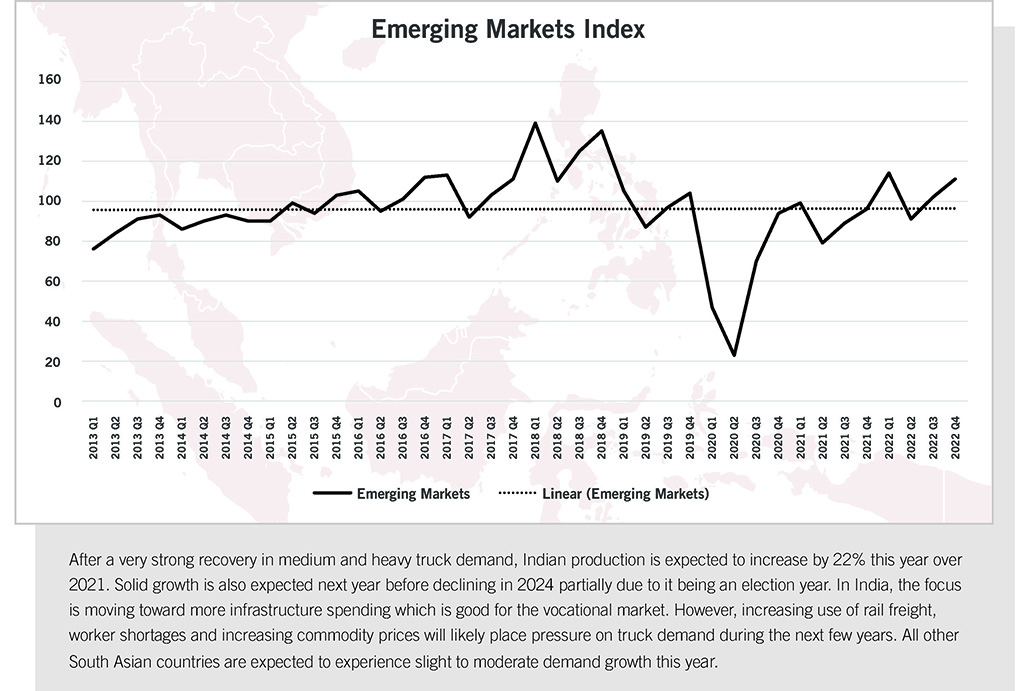

South Asia

After a very strong recovery in medium and heavy truck demand, India’s production is expected to increase by 22% this year over 2021. Solid growth is also expected next year before declining in 2024 partially due to it being an election year. In India, the focus is moving toward increase in infrastructure spending which is good for the vocational market. However, the increasing use of rail freight, worker shortages and increasing commodity prices likely will place pressure on truck demand during the next few years. All other South Asian countries are expected to experience slight to moderate demand growth this year.

South America

After exceedingly elevated levels of MHCV production in Brazil last year, overall production in South America is expected to increase by 3.2% this year. The increased truck capacity from last year’s high production along with the risk of higher interest rates in the second half of 2022 and some impact in agriculture due lack of fertilisers will pressure production levels throughout the year. Emission regulation Proconve 8 or P8, equivalent to Euro VI, is required by January 2023. The legislation considers MHV to be all CV vehicles above 3.8 tonnes. The additional vehicle cost of the P8 emission technology will have a negative impact on demand next year.

Japan and Korea

Medium and heavy commercial vehicle production in Japan and South Korea is expected to increase by 3.6% this year over 2021. Concerns surrounding a slowing global economy along with continued supply chain disruptions will impact vehicle demand throughout the remainder of this year and into 2023. Japan and South Korea have a sizeable portion of the global vehicle export market, most notably in the ASEAN region.

Greater China

Medium and heavy commercial vehicle production is expected to decline by 30% this year, driven by a slowing economy and the affects from the pandemic-related lockdowns. The slowdown continues to impact global supply chains. China is also carrying a significant amount of debt and home sales, which account for approximately 30% of GDP, and are declining sharply. Home sales declined 34.5% in the first five months of this year compared with the same period last year. Many property developers are defaulting due to large unsustainable debts. China’s banking system is also under pressure and is showing signs of a contracting economy.

The next update of the Power Systems Research TPI will be in October 2022 and will reflect changes in the TPI during Q3 2022.